Pay less for the same

car loan.

AI does the work.We don't pay human brokers.Neither do you.

No credit score impact · no obligation

- Wide panel of lenders

- AI powered, human-verified

- 24/7 availability

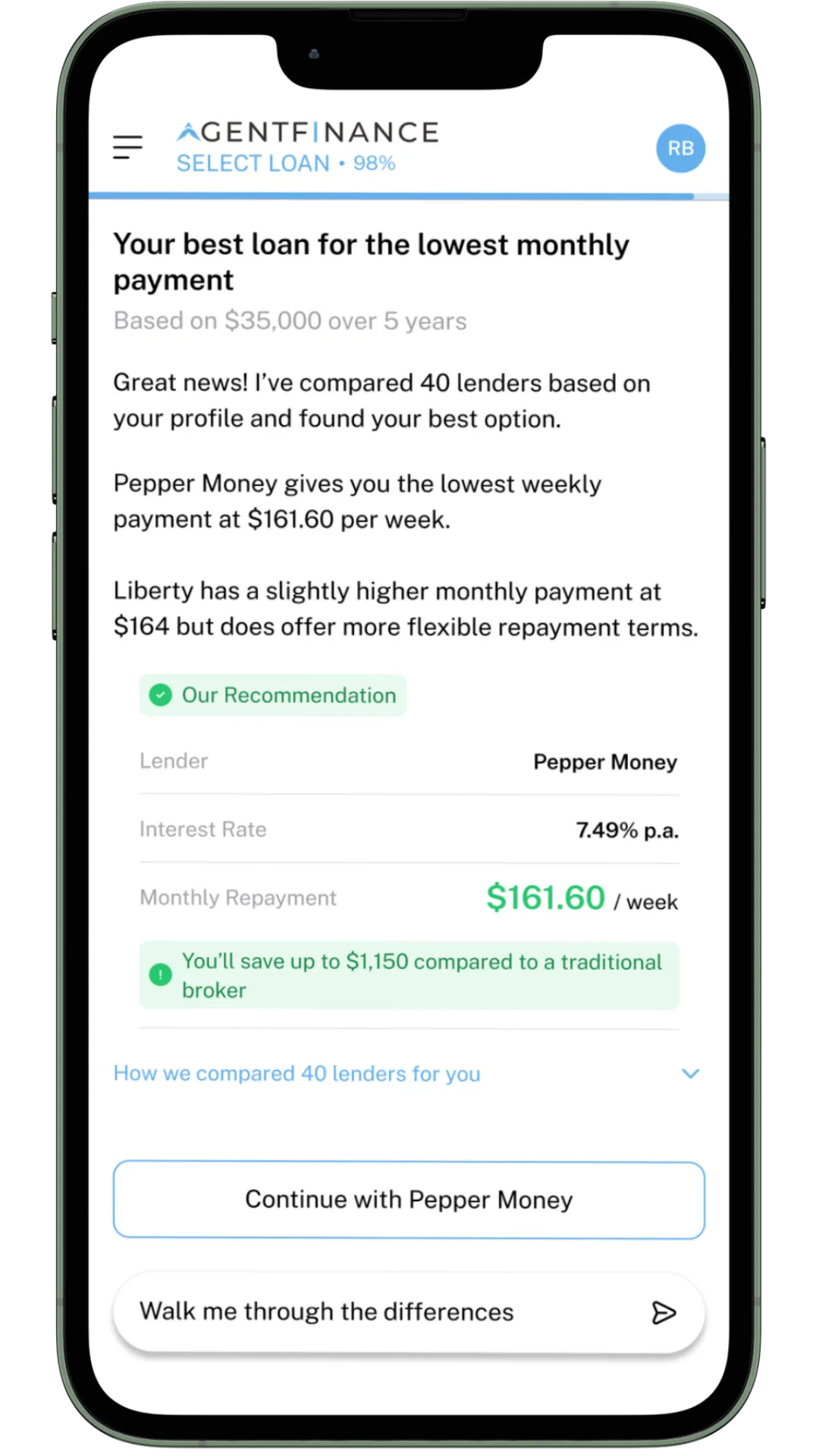

Why your car loan costs less

Agent Finance

$699 flat fee

No commission

Typical broker or dealer

Fees up to $2,500

plus commission up to 5%

Source: ASIC Report 832, June 2026. Broker and dealer fee caps and case studies as published in the report. Commission range reflects current lender broker commission schedules. Figures as at July 2026.

ASIC reviewed more than 350,000 car loans this year. Depending on the lender, the broker or dealer arranging your loan can charge an establishment fee of up to $2,500. In one of ASIC's case studies, a borrower paid $4,503 to a broker on a single loan.

Then there's commission, charged on top of that fee. Lenders pay the broker or dealer a percentage of your loan, built into your rate: typically 3%, and it can run to 5%. On a $50,000 loan, even the typical 3% is $1,500. However they mix it, you pay it.

Our fee is $699. Flat, published, whatever you borrow. No hidden commission. No fee if your loan doesn't proceed. Same lenders. Same loans. Less cost.

Right. Let's talk about why you can trust a koala with your car loan.

I'm Fin. I'm the AI that runs Agent Finance. Yes, I'm also a koala in a suit. The koala is marketing. The AI is real.

Here's what I do. You tell me about the car and about you. I search a wide panel of lenders, match your profile to the ones most likely to say yes, and handle everything through to the money reaching the seller. A licensed broker checks every deal I put together before it goes anywhere.

Arranging loans is time-consuming and costly for humans. It's not for an AI. I pass those savings directly on to you.

I can't earn more by giving you a worse deal. It's not in my code.A human broker earns more when your loan costs more. I earn $699, whatever you borrow, whichever lender you end up with. You come first. It's hard-coded in my DNA.

So if you can get a better deal somewhere else, take it.I protect your credit score like it's mine. And I'm here at 9pm when you finally get time to sort this out.

No credit score impact · no obligation

One conversation, from first quote to cash at bank.

Get a quote in seconds.

Tell me the vehicle price, any trade-in or deposit, and your term. In less than a minute, I'll show you your likely repayments, based on live lender rates. No documents. No mark on your credit file. No obligation.

Your shortlist.

Then I ask what a good broker would ask. About ten minutes to work out which loans genuinely suit you, ending with the best offers I find and which one fits you. If none do, I'll tell you that too.

Same conversation to settlement.

Application, documents, lender questions, approval, settlement: all in the same thread. I don't keep business hours, so nothing waits for Monday. A licensed broker checks the deal before it goes to the lender. The money lands with the seller. You get the car.

And after settlement I don't disappear. When the next car happens, or the next question, I'm here.

No credit score impact · no obligation

Australian Credit Licence 384 704

See how it worksI protect your credit score like it's mine.

Every lender you apply with leaves a mark on your credit file, whether you get the loan or not. One mark is fine. A few marks close together and lenders start reading them as desperation. That means more knock-backs, which means more applications, which means more marks. People get trapped in that loop for years, paying higher rates the whole way, and most never find out why.

Here's how it happens. You apply direct and get declined, so you try somewhere else: two applications on your file. You put your details into a comparison site and your application can go to several lenders at once. Some brokers do the same, hoping one says yes. Every one of those is recorded.

I work in a different order. Soft check first: I see your real credit position, the same information lenders see, without adding an application to your file. Then I match you against lender rules before anything is submitted, and apply once, where you're likely to be approved. When I do apply, it counts.

Protecting your credit file is half of what a good broker is for. I do it without the commission. Here's exactly how

Four ways to finance a car.

Three of them don't have to put you first.

By law, mortgage brokers must act in your best interests. Nobody arranging your car loan has to.

Dealership finance

- How they make money

- A fee plus commission, usually 3 to 5% of your loan, built into your rate

- What you're shown

- Their lenders' rates, not the market

Comparison sites

- How they make money

- Paid by lenders for every customer they send

- What you're shown

- The lenders that pay to be listed

Traditional broker

- How they make money

- A fee plus commission, usually 3 to 5% of your loan, built into your rate

- What you're shown

- Depends who you get. Some find you the best deal. Some don't

Agent Finance

- Your best interests

- Hard-coded to put you first

- How I make money

- $699 flat. Same fee, any loan, any lender.

- What you're shown

- The best offers I find, and what I earn: $699

AI removes the cost and the conflict.

Whoever you are, you get the same broker.

Human brokers pick their battles. Big loans and clean credit get the callbacks; everyone else gets the voicemail. I don't have a shortlist. $15,000 or $150,000, salaried or self-employed, first car or fifth: same process, same effort, same $699.

Self-employed and ABN

Car finance without the income verification headaches

Bad credit

I'll show you where you actually stand, and what's realistic

First car

A straight explanation of your first loan, start to finish

Uber and gig workers

Finance built around variable income

EV buyers

Green loans and EV finance, explained

Used cars

Finance for used and pre-owned vehicles

I've worked inside Australia's largest car finance brokers. The service is genuine — but it takes a lot of people, a lot of process, and that cost gets passed to you in ways most people never see. I built Agent Finance to deliver the same quality with AI doing the heavy lifting, so you don't have to pay for the overheads.

Frequently Asked Questions About Car Finance in Australia

Ready to pay less for your car loan?

Fin is here to help you 24/7

Australian Credit Licence 384 704